Written by R.W. Baird analyst David J. Manthey, CFA with Quinn Fredrickson, CFA 9/4/20

Key Takeaway:

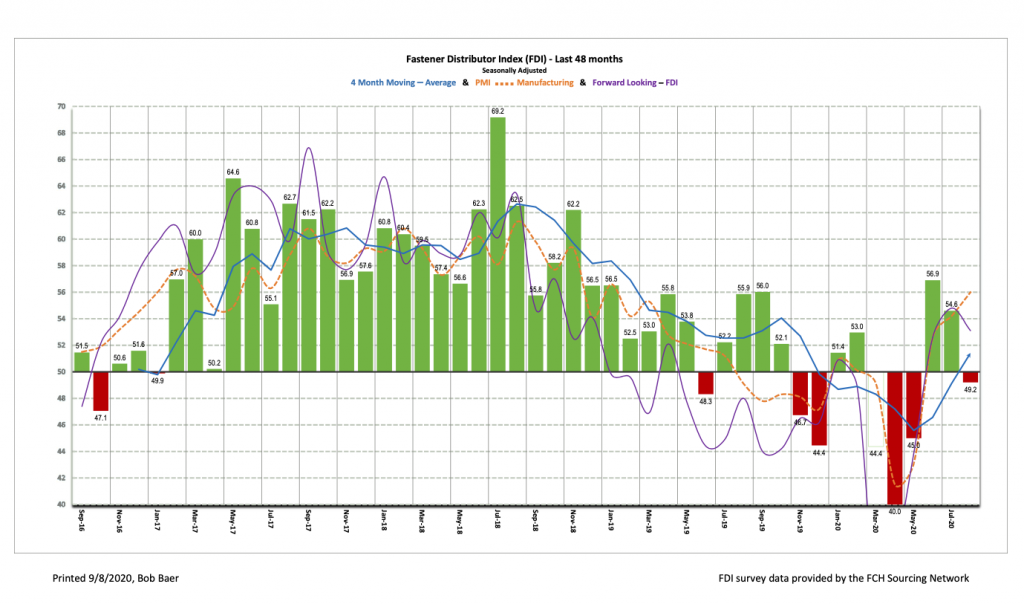

The seasonally adjusted Fastener Distributor Index (FDI) for August was 49.2, implying relatively stable momentum with July (near a neutral 50 reading). Looking at the drivers of the overall m/m moderation in the FDI, a decrease in the sales index was the biggest drag on the overall index. Looking forward, the Forward-Looking Indicator (FLI) was relatively steady, staying in the ~53-54 range seen consistently over the past three months (August 53.3). Taking the FDI and FLI together, in our view, we believe this indicates August fastener market conditions showed relative stability in trends after several consecutive months of strong m/m improvement.

Key Points:

August FDI shows steady momentum after two consecutive months of strong improvement. The seasonally adjusted August FDI (49.2) came in near a neutral reading of 50, suggesting August fastener markets were relatively stable with July. After two consecutive months of fairly sharp improvements in the FDI, naturally the rate of improvement stalled some in August. The seasonally adjusted sales index, specifically, was the main driver of this moderation (July FDI 54.6), as the sales index cooled to 47.6 off a very strong 79.2 last month. Pricing was also steady for most respondents m/m.

FLI remains in a narrow band for third straight month. The seasonally adjusted FLI was 53.1, the third consecutive month of FLI readings in the ~53-54 range. We view this as consistent with a market that continues to gradually improve modestly, albeit with the pace of improvement flattening out. Respondents again indicated they feel more optimistic than pessimistic about the six-month outlook on balance (however slightly less so than last month), while decreasing customer inventory levels could possibly signal a need for customer re-stocking in the future, a positive sign for future activity levels. Net, we believe the FDI should see continued modest expansionary readings in the near-term following the temporary dip this month to just below-50.

Stable hiring sentiment. The FDI employment index registered a 46.1 reading, a modest improvement from last month’s 44.3. After an elevated month of hiring in June (presumably as additional customer facilities opened and lingering state/local government restrictions were eased), July and August have both been more stable months for hiring. Looking at the broader economy, while the unemployment rate is still elevated (8.4% as of August), we’ve now seen four consecutive months of better-than-expected job gains as businesses continue to re-open and demand gradually recovers, including +1.4 million jobs added in August. That said, the ongoing recovery in the employment situation (and the broader economy) remains on tenuous ground, subject to the trajectory of the virus and/or government shutdowns.

Respondent commentary slightly more positive on balance. We noticed more respondent commentary indicating higher levels of activity and an improved outlook than those expressing dissatisfaction with current activity levels. One respondent summarized it by saying, “More activity,” while another commented, “Our fiscal year ended July 31st and we experienced a record year in sales, and in August 2020, we just had the highest dollar amount in sales in 13 months.” Lastly, others expressed frustration in being unable to secure enough labor (“We need more humans in our business!”), which we view as a positive sign that this particular respondent is struggling to keep up with demand, while another said, “The best is yet to come.” More cautious commentary included: “The slowing trend with incoming orders has us concerned concerning the next three months,” and “Down 25% from last year’s August. Down 11% YTD compared to the same period last year. Very, very slow month.” Attitudes about expected activity levels over the next six months compared to today are more positive than negative on balance, however, with 53% of participants expecting higher activity levels and only 24% expecting lower.

Fastenal reported 2.5% overall August daily sales growth vs. our +0.0% estimate, again boosted by significant demand for safety/PPE (+35% y/y). Excluding safety products, underlying sales were -4.2% y/y, showing modest m/m improvement vs. July’s -4.6% y/y but coming in slightly below our -3.1% estimate. Similar to an FDI reading that indicated relatively stable fastener markets, FAST’s fastener sales were stable m/m at -7.3% (July -7.5%). Looking forward, September safety product sales will likely continue to benefit from surge orders, although we are conservatively assuming m/m moderation (our September estimate is +10% y/y vs. August +35%). We expect underlying momentum in fastener products and other non-fastener products to continue to moderately improve, albeit offset by two additional selling days m/m relative to normal seasonality, which optically places downward pressure on daily sales growth rates. As such, we are modeling overall daily sales – 3.7% in September, which will be reported with FAST’s 2Q20 report (10/13).

Risk Synopsis

Industrial Distribution: Risks include economic sensitivity, pricing power, online pressure/competitive threats, global sourcing, and exposure to durable goods manufacturing.

For the full FDI report for August 2020, with graphs and disclosures, Click-here.