Written by R.W. Baird analyst David J. Manthey, CFA with Quinn Fredrickson, CFA 11/6/20

Key Takeaway:

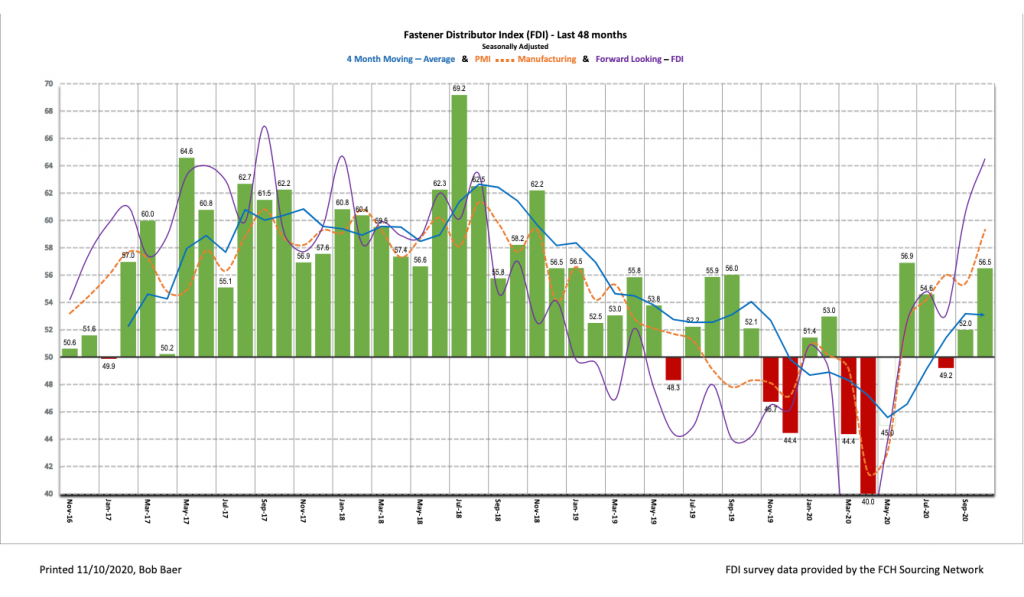

The seasonally adjusted Fastener Distributor Index (FDI) for October was 56.5, improving for the second

consecutive month. Nearly all components of the FDI showed m/m improvement. Looking forward, the

Forward-Looking Indicator (FLI) also showed nice improvement, reaching the highest levels since January

2018 at 64.5. Taking the FDI and FLI together, in our view, we believe this indicates October fastener

market conditions showed m/m improvement at a greater rate than September.

About the Fastener Distributor Index (FDI). The FDI is a monthly survey of North American fastener

distributors, conducted with the FCH Sourcing Network and Baird with support from the National Fastener

Distributors Association. It offers insights into current fastener industry trends/outlooks. Similarly, the

Forward-Looking Indicator (FLI) is based on a weighted average of four forward-looking inputs from the FDI

survey. This indicator is designed to provide directional perspective on future expectations for fastener

market conditions. As diffusion indexes, values above 50.0 signal strength, while readings below 50.0 signal

weakness. Over time, results should be directly relevant to Fastenal (FAST) and broadly relevant to other

industrial distributors such as W.W. Grainger (GWW) and MSC Industrial (MSM).

Key Points:

October FDI shows momentum improved m/m vs. September and at a faster rate. The seasonally

adjusted October FDI (56.5) remained well into expansionary territory and improved m/m at a faster rate

than September. Nearly all FDI components saw improvement but gains were most significant across the

seasonally adjusted sales index, which came in at 65.1 vs. 60.8 last month. Pricing was mostly stable with

last month.

FLI continues recent upward march. The seasonally adjusted FLI was 64.5, improving nicely from

September’s 60.6. This was also the highest FLI reading recorded since January 2018. We view this

breakout as a positive sign going forward, as low customer inventories, coupled with a continued slightly

more optimistic tone around hiring, could bode well for near-term prospects. Net, we believe the FDI

should see expansionary readings in the near term, implying additional m/m improvement in market

conditions ahead even as trends on a y/y basis for many respondents may remain down.

Hiring sentiment continues to moderately improve. The FDI employment index registered a 58.3

reading vs. September 53.7. Looking at the broader economy, despite a continued recovery in the labor

market, the unemployment rate remains elevated (6.9% as of October). The October jobs report showed

slightly better than expected jobs added (+630,000 vs. economists’ consensus of ~600,000), but the

economy remains down about 10 million jobs from pre-pandemic levels. This was the seventh straight

month of net gains but also the fifth consecutive month of decelerating additions.

Respondent commentary mostly focused on election. The Presidential election was not surprisingly the

main area of focus for respondents this month. One respondent indicated, “The future is hinged on two

things not in anyone’s control: the general election and potential spikes in COVID globally,” while another

commented, “I have a feeling this survey would be vastly different if you held it on 11/4 versus 11/2.”

There were also comments that suggested demand continues to strengthen. Per one participant,

“Business is definitely improving and [our] expectation is to stay on a growth pattern but at a slower rate

than what some industry economic sources are saying. What happens with COVID the next few months

can be a major factor on the positive growth [we’re] experiencing currently.” Attitudes about expected

activity levels over the next six months compared to today remain more positive than negative on

balance, however, with 72% of participants expecting higher activity levels and only 6% expecting lower.

Fastenal reported 4.1% overall October daily sales growth vs. our +0.7% estimate, again boosted by

significant demand for safety/PPE (+32% y/y). Excluding safety products, underlying sales were -1.6% y/y,

showing continued sequential improvement relative to September’s -3.5% y/y. Similar to an FDI reading

that indicated improving fastener markets sequentially, FAST’s fastener sales were better m/m at -4.7%

(September -6.1%). Looking forward, November safety product sales will likely see continued elevated

demand, although we are conservatively assuming m/m moderation (our November estimate is +10%

y/y vs. October +32%). We expect underlying momentum in fastener products and other non-fastener

products to be mostly steady with October. Putting it all together, we are modeling overall daily sales –

0.2% y/y in November, which will be reported December 4.

Risk Synopsis

Fastenal: Risks include economic sensitivity, pricing power, relatively high valuation, secular gross margin

pressures, success of vending and on-site initiatives, and ability to sustain historical growth.

Industrial Distribution: Risks include economic sensitivity, pricing power, online pressure/competitive

threats, global sourcing, and exposure to durable goods manufacturing.

For the full FDI report for October 2020, with graphs and disclosures, Click-here.