Written by R.W. Baird analyst David J. Manthey, CFA with Quinn Fredrickson, CFA 3/4/21

Key Takeaway:

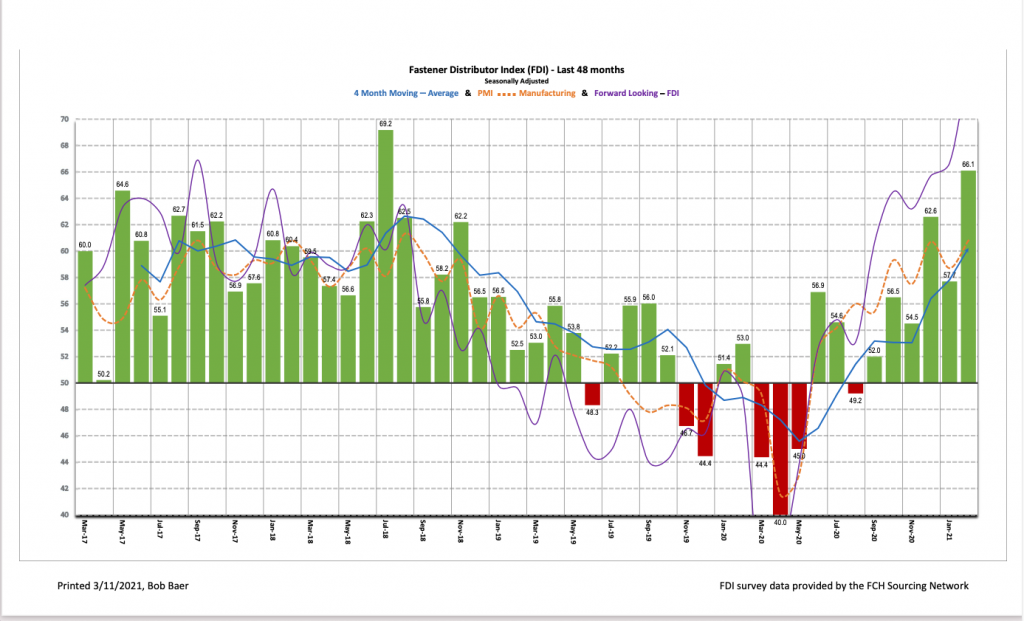

The seasonally adjusted Fastener Distributor Index (FDI) for February saw strong m/m improvement with a reading of 66.1. The sales index surged as two-thirds of respondents saw sales that were above seasonal expectations in a normally seasonally softer month. The Forward-Looking Indicator (FLI) also saw a significant m/m acceleration, reaching a record high of 73.9 signaling additional expansionary demand conditions in the months ahead. Net, we believe February was a strong month for most fastener distributors relative to expectations.

About the Fastener Distributor Index (FDI). The FDI is a monthly survey of North American fastener distributors, conducted with the FCH Sourcing Network and Baird with support from the National Fastener Distributors Association. It offers insights into current fastener industry trends/outlooks. Similarly, the Forward-Looking Indicator (FLI) is based on a weighted average of four forward-looking inputs from the FDI survey. This indicator is designed to provide directional perspective on future expectations for fastener market conditions. As diffusion indexes, values above 50.0 signal strength, while readings below 50.0 signal weakness. Over time, results should be directly relevant to Fastenal (FAST) and broadly relevant to other industrial distributors such as W.W. Grainger (GWW) and MSC Industrial (MSM).

Key Points:

FDI sees nice m/m expansion. The seasonally adjusted February FDI (66.1) saw solid growth relative to last month’s 57.7 reading. A robust 69% of respondents saw better than seasonally expected sales in February, which is consistent with levels seen over the last three months. Inflationary pressures, particularly in steel and freight costs, continue to be felt by many respondents. Additionally, supplier lead times remain very extended, leaving some respondents concerned about their ability to meet future demand.

FLI surges to record high. The seasonally adjusted FLI was 73.9, surging vs. last month’s already very strong 66.7 reading and marking a new all-time high for the index. All four components of the FLI (employment, respondent inventories, customer inventories, and six-month outlook) turned more bullish relative to January. The customer inventory index is perhaps most notable in powering exceptionally strong FLI results. A record 69% of respondents consider customer inventory levels to be currently too low, implying some restocking is needed ahead, which should be bullish for future demand conditions. With the FLI well above 50, customer inventories getting increasingly low, and respondents continuing to forecast favorable six-month outlooks, we believe the FDI should see additional expansionary readings ahead, implying continued improvement particularly as y/y comparisons ease significantly next month.

Employment levels were slightly higher m/m. The FDI employment index registered a 67.1 reading this month vs. 64.3 last month. Forty-three percent of respondents saw employment levels as above seasonal expectations in February compared to 34% in January. Looking at the broader economy, despite a continued gradual recovery in the labor market, the unemployment rate remains elevated (6.3% as of January), and even more so when including discouraged and part-time workers (11.1% unemployment). The January jobs report showed a very modest increase in jobs (+49,000) that was in line with economists’ expectations (+50,000), but still showed a net reduction over the last two months considering December’s 227,000 jobs lost.

Supply chain constraints remain key area of focus for respondents. For the second consecutive month, nearly every comment touched on raw material inflation and logistics issues. Congestion at the ports, container shortages, and weather challenges are causing significant logistics disruptions. Per one respondent, “FedEx and freight companies lost some big shipments, otherwise we would have been much higher. Blaming the icing to the Midwest as the reason why and oh yeah, China virus too.” Rapid spikes in raw material inflation also continues to cause headaches for many respondents. As one comment summarized, “Material price spikes [are] unreal, in some cases 30-60% higher. Freight costs from overseas continue to be as challenging as [is] getting product out of the port in Long Beach. Lead times are climbing as overseas is bombarded with orders from the Big Boys, and domestic supplier lead times are skyrocketing due to [an] influx of business and suppliers covering the gap from overseas. Meanwhile getting material pricing domestic can take up to two weeks due to shortages. Quite a mess right now.” Similarly, another respondent said, “Steel is getting more expensive and much more difficult to get. Supply vs demand is a genuine concern .” Manufacturers continue to struggle in meeting the elevated demand, prompting one respondent to say, “Demand is substantial at this time, while supply is depleting and manufacturer lead times are extending further.”

Fastenal’s 1.5% overall February daily sales growth trailed our +4.5% estimate, including a significant drag from unfavorable weather conditions (-2.6-3%) and soft non-residential construction demand (-14.4%). Safety growth remained very strong at +17.6%, although growth has clearly moderated as FAST begins comping 2020 pandemic safety sales. Excluding safety products, underlying sales decelerated to -2.2% y/y. Turning to fasteners specifically, FAST’s fastener sales were slightly weaker m/m at -2.1% (January -0.2%).

Risk Synopsis

Fastenal: Risks include economic sensitivity, pricing power, relatively high valuation, secular gross margin pressures, success of vending and on-site initiatives, and ability to sustain historical growth.

Industrial Distribution: Risks include economic sensitivity, pricing power, online pressure/competitive threats, global sourcing, and exposure to durable goods manufacturing.

For the full FDI report for February 2021, with graphs and disclosures, Click-here.